Self-Funding

People pay for long term care in different ways. This can include using your or your family's personal resources, including savings and investments, or other assets such as your home.

When determining whether you should self-fund or purchase long term care insurance, it's important to look at your current and future savings and assets to determine how much you can afford to spend, specifically for long term care. What may work for a person with few resources, a modest income, and a goal of staying off Medicaid will be very different from someone with a larger amount of assets and income.

You should also consider the cost of long term care and how long you think you will need it.

Paying for long term care

Below are the costs in today's dollar. Is this something that you can afford to pay from your own savings if you need care now?

| National Average Annual Cost of Care1 | ||

|---|---|---|

| Home Care | $51,480* | |

| Assisted Living | $66,132 | |

| Nursing Home | $112,420 | |

| Average | $76,677 | |

![]()

Use our Cost of Care Tool to find the average cost of care in your area.

Length of Care

33

Months

is the average time a FLTCIP

claimant receives benefits

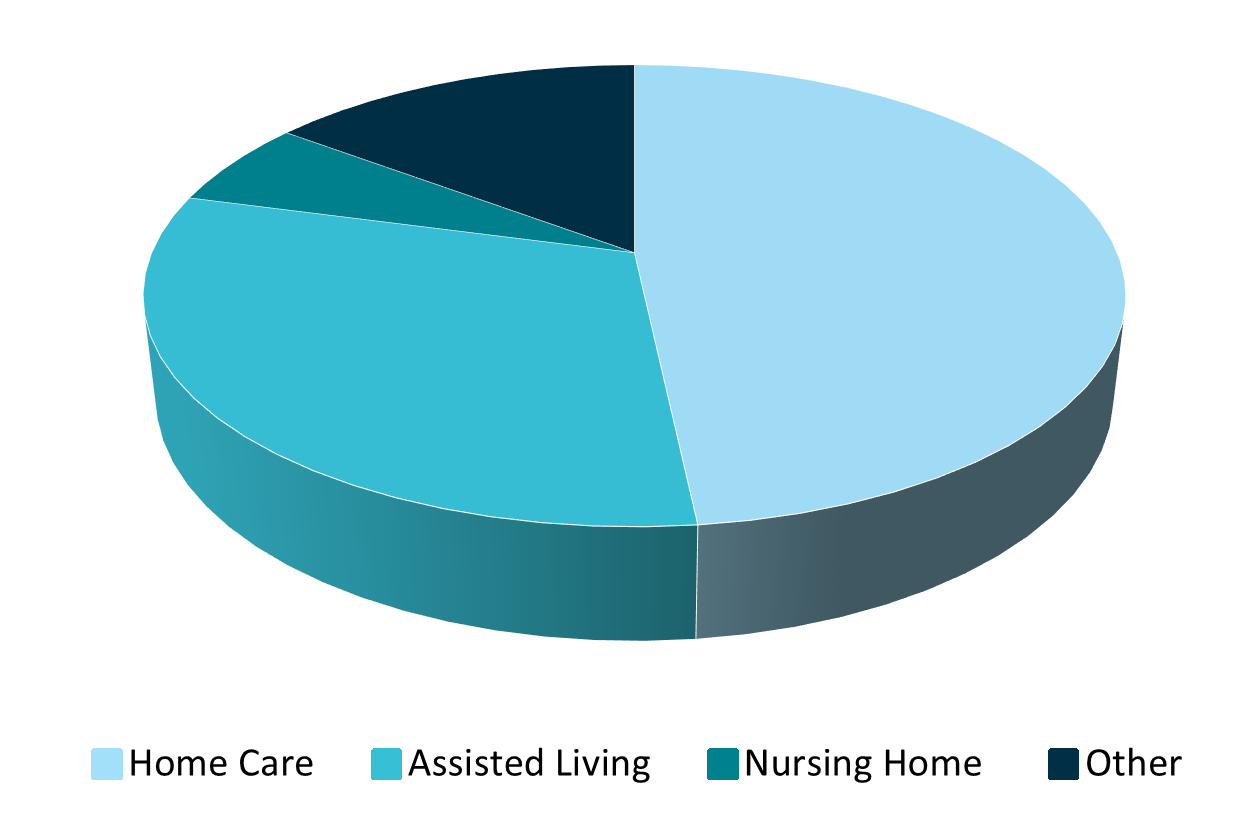

Type of Care

These figures are as of December 2025.

Saving for long term care

Because the cost of long term care can be expensive, paying for it should be considered as part of your overall financial plan. And, the best time to think about how much you might need is well before you need it, while you're still in good health.

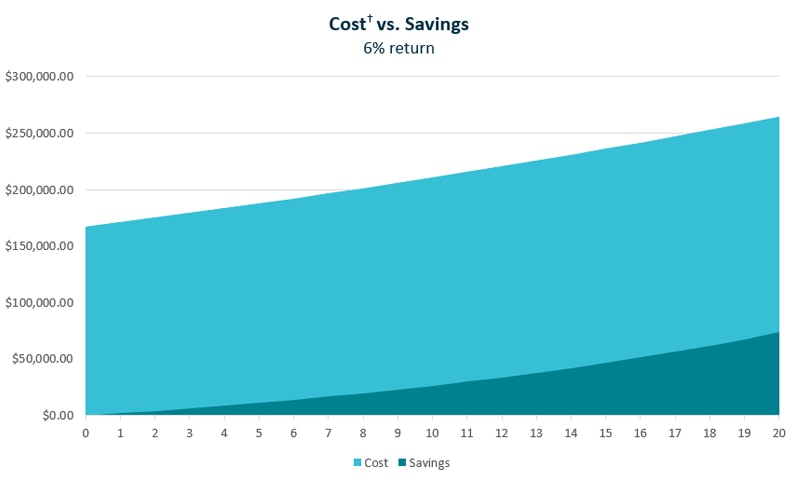

Here are some examples to show the cost of care over time compared to what you may be able to save.

The graph below shows the cost of care over 20 years compared to if you started saving $2,000 every year now, at a 6% return. The cost is based on the average annual cost of all three types of care, $76,677 (see above), multiplied by the average length of time care is typically received, 2.5 years (see above). The increase in cost is based on an annual rate of inflation of 2.54%.†

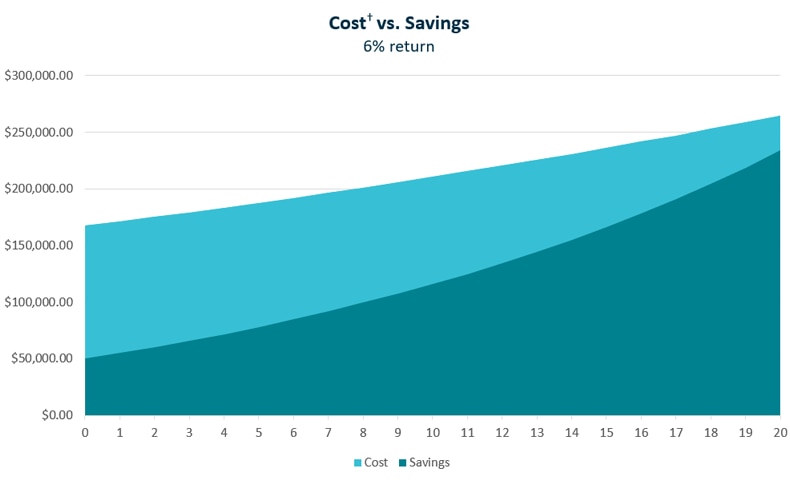

This next graph uses the same variables as the one above but assumes you have already accumulated $50,000 worth of savings specifically to pay for long term care.

The decision on whether or not to purchase long term care insurance is an important financial decision. The costs and comparison graphs above are meant to provide general guidelines. Actual costs and projected savings may be different. We recommend that you consult with a financial advisor for specific advice about your long term care planning.